An important signal in the emergence of crypto-currencies and blockchain-distributed-ledger technologies – this one from the Bank for International Settlements.

An important signal in the emergence of crypto-currencies and blockchain-distributed-ledger technologies – this one from the Bank for International Settlements.

This is a long read – useful for anyone interested in the future of currency. The article is an excellent summary of the current situation and has a very good list of current efforts to develop e-currencies. The next 10-15 years will definitely be a change in conditions of change regarding the medium of accounting for value creation and exchange.

CADcoin is an example of a wholesale CBCC. It is the original name for digital assets representing central bank money used in the Bank of Canada’s proof of concept for a DLT-based wholesale payment system. CADcoin has been used in simulations performed by the Bank of Canada in cooperation with Payments Canada, R3 (a fintech firm), and several Canadian banks but has not been put into practice.

Sweden has one of the highest adoption rates of modern information and communication technologies in the world. It also has a highly efficient retail payment system. At the end of 2016, more than 5 million Swedes (over 50% of the population) had installed the Swish mobile phone app, which allows people to transfer commercial bank money with immediate effect (day or night) using their handheld device. The demand for cash is dropping rapidly in Sweden right-hand panel). Already, many stores no longer accept cash and some bank branches no longer disburse or collect cash.

New cryptocurrencies are emerging almost daily, and many interested parties are wondering whether central banks should issue their own versions. But what might central bank cryptocurrencies (CBCCs) look like and would they be useful? This feature provides a taxonomy of money that identifies two types of CBCC – retail and wholesale – and differentiates them from other forms of central bank money such as cash and reserves. It discusses the different characteristics of CBCCs and compares them with existing payment options.

In less than a decade, bitcoin has gone from being an obscure curiosity to a household name. Its value has risen – with ups and downs – from a few cents per coin to over $4,000. In the meantime, hundreds of other cryptocurrencies – equalling bitcoin in market value – have emerged. While it seems unlikely that bitcoin or its sisters will displace sovereign currencies, they have demonstrated the viability of the underlying blockchain or distributed ledger technology (DLT). Venture capitalists and financial institutions are investing heavily in DLT projects that seek to provide new financial services as well as deliver old ones more efficiently. Bloggers, central bankers and academics are predicting transformative or disruptive implications for payments, banks and the financial system at large.

Lately, central banks have entered the fray, with several announcing that they are exploring or experimenting with DLT, and the prospect of central bank crypto- or digital currencies is attracting considerable attention. But making sense of all this is difficult. There is confusion over what these new currencies are, and discussions often occur without a common understanding of what is actually being proposed. This feature seeks to provide some clarity by answering a deceptively simple question: what are central bank cryptocurrencies (CBCCs)?

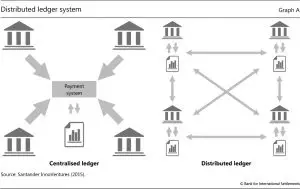

To that end, we present a taxonomy of money that is based on four key properties: issuer (central bank or other); form (electronic or physical); accessibility (universal or limited); and transfer mechanism (centralised or decentralised). The taxonomy defines a CBCC as an electronic form of central bank money that can be exchanged in a decentralised manner known as peer-to-peer, meaning that transactions occur directly between the payer and the payee without the need for a central intermediary. This distinguishes CBCCs from other existing forms of electronic central bank money, such as reserves, which are exchanged in a centralised fashion across accounts at the central bank. Moreover, the taxonomy distinguishes between two possible forms of CBCC: a widely available, consumer-facing payment instrument targeted at retail transactions; and a restricted-access, digital settlement token for wholesale payment applications.

…Looking beyond the immediate horizon, many industry participants see significant potential for DLT to increase efficiency and reduce reconciliation costs in securities clearing and settlement. One potential benefit of DLT-based structures is immediate clearing and settlement of securities, in contrast to the multiple-day lags that currently exist when exchanging cash for securities (and vice versa). Progress in this direction was recently achieved by a joint venture between the Deutsche Bundesbank and Deutsche Börse, which developed a functional prototype of a DLT-based securities settlement platform that achieves delivery-versus-payment settlement of digital coins and securities (Deutsche Bundesbank (2016)).

Leave a Reply